As How to Access Your Home Equity in Australia: A Guide to Line of Credit takes center stage, this opening passage beckons readers with casual formal language style into a world crafted with good knowledge, ensuring a reading experience that is both absorbing and distinctly original.

Providing a detailed insight into the intricate process of accessing home equity in Australia through a line of credit, this guide aims to equip readers with valuable information to navigate this financial landscape effectively.

Understanding Home Equity and Line of Credit

Home equity and line of credit are important concepts to understand when it comes to unlocking the value of your property for financial purposes.

Home Equity

Home equity is the difference between the current market value of your property and the amount you owe on your mortgage. It represents the portion of your home that you truly own.

- Home Equity = Market Value of Property - Mortgage Owed

Line of Credit

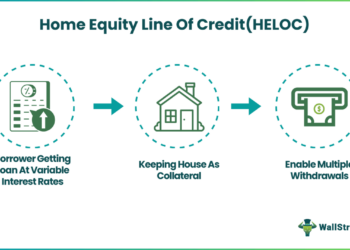

A line of credit is a type of loan that allows you to borrow money using the equity in your home as collateral. It works similarly to a credit card, where you have a maximum credit limit that you can borrow against as needed.

- With a line of credit, you can borrow up to a certain limit and only pay interest on the amount you actually use.

- You can access funds as needed and repay them on a flexible schedule.

Difference Between Home Equity Loans and Lines of Credit

While both home equity loans and lines of credit allow you to use the equity in your home for borrowing, there are key differences between the two:

- Home Equity Loans: Provide a lump sum of money upfront, with a fixed interest rate and regular monthly payments.

- Lines of Credit: Offer a revolving credit line, allowing you to borrow, repay, and borrow again up to a certain limit, with variable interest rates.

Eligibility and Requirements

To access your home equity in Australia, there are specific eligibility criteria that you need to meet. Additionally, there are certain requirements and documentation needed when applying for a line of credit. Understanding the credit score requirements is also crucial when considering obtaining a home equity line of credit.Eligibility Criteria

- Ownership of a property: You must be the owner of a property in Australia to access home equity.

- Equity in your home: You need to have built up equity in your property through mortgage repayments or an increase in property value.

- Income and affordability: Lenders will assess your income and financial stability to ensure you can repay the line of credit.

- Credit history: A good credit history is essential to demonstrate your ability to manage debt responsibly.

Documentation Needed

- Proof of identity: This includes a valid ID such as a driver's license or passport.

- Property documents: You will need to provide documents related to the ownership of the property.

- Income verification: Pay stubs, tax returns, or bank statements to prove your income.

- Financial statements: Lenders may require information on your assets and liabilities.

Credit Score Requirements

- Your credit score plays a significant role in determining your eligibility for a home equity line of credit.

- Generally, a credit score of 620 or higher is considered good for securing a line of credit.

- A higher credit score may lead to better terms and lower interest rates on the line of credit.

Pros and Cons of Using Home Equity

Using home equity through a line of credit can be a beneficial financial strategy, but it also comes with risks that need to be carefully considered. Let's explore the advantages and disadvantages of tapping into your home equity.Advantages of Using Home Equity

- Access to Lower Interest Rates: Home equity lines of credit typically offer lower interest rates compared to other forms of credit, making it a cost-effective borrowing option.

- Flexible Withdrawals: With a line of credit, you have the flexibility to access funds as needed, allowing you to borrow only what you require at a given time.

- Tax Deductible Interest: In some cases, the interest paid on a home equity line of credit may be tax deductible, providing potential tax benefits.

- Potential for Home Value Appreciation: By investing borrowed funds back into your home, you may increase its value over time, potentially leading to a higher return on investment.

Risks Associated with Accessing Home Equity

- Risk of Losing Your Home: Using your home as collateral means that failure to repay the loan could result in foreclosure, putting your property at risk.

- Variable Interest Rates: Home equity lines of credit often come with variable interest rates, meaning your monthly payments could fluctuate based on market conditions.

- Increased Debt Burden: Accessing home equity can lead to increased debt levels, which may become challenging to manage if financial circumstances change.

Comparison to Other Financing Options

- Flexibility Compared to Traditional Loans: Unlike traditional loans with fixed terms, a line of credit offers more flexibility in terms of borrowing and repayment, aligning with your evolving financial needs.

- Lower Interest Rates Compared to Credit Cards: Home equity lines of credit generally have lower interest rates than credit cards, making them a more cost-effective option for large expenses.

- Higher Risk Than Personal Loans: While personal loans do not require collateral, they often have higher interest rates than home equity lines of credit, making them less attractive for borrowers looking for lower cost financing.

Steps to Access Home Equity in Australia

When it comes to accessing your home equity in Australia, there are specific steps you need to follow to apply for a line of credit and get the funding you need. Understanding the process of getting your home appraised for equity assessment and the timeline for approval and funding is essential for a successful outcome.Applying for a Line of Credit

- Research Lenders: Start by researching different lenders who offer home equity lines of credit in Australia.

- Submit Application: Once you have chosen a lender, submit your application along with all the required documents.

- Wait for Approval: The lender will review your application, credit history, and home equity to determine if you qualify for a line of credit.

Getting Your Home Appraised

- Hire an Appraiser: The lender will require an appraisal of your home to assess its current market value.

- Appraisal Process: The appraiser will visit your property, evaluate its condition, size, location, and comparable properties in the area to determine its value.

- Receive Appraisal Report: Once the appraisal is complete, you will receive a report detailing the assessed value of your home.

Timeline for Approval and Funding

- Approval Process: The approval process for a home equity line of credit can take a few weeks as the lender reviews your application and supporting documents.

- Final Approval: Once your application is approved, you will receive final approval for the line of credit.

- Funding: After final approval, the funds from your home equity line of credit will be disbursed to you based on the agreed terms.

Managing and Repaying Home Equity

Effectively managing and repaying home equity funds is crucial to make the most out of a line of credit while avoiding financial pitfalls.

Repayment Options for Home Equity Lines of Credit

When it comes to repaying a home equity line of credit, borrowers typically have several options to choose from:

- Interest-Only Payments: Borrowers can choose to make interest-only payments during the draw period, which can provide flexibility but may result in higher payments later on.

- Principal and Interest Payments: Making payments towards both the principal amount and the interest accrued can help pay off the debt faster and reduce overall interest costs.

- Balloon Payment: Some lenders may require a balloon payment at the end of the draw period, which is a large lump sum payment to pay off the remaining balance.

Consequences of Defaulting on Payments

Defaulting on payments for a home equity line of credit can have serious consequences, including:

- Damage to Credit Score: Missing payments or defaulting can negatively impact your credit score, making it harder to borrow in the future.

- Foreclosure: If you fail to repay the loan, the lender may foreclose on your home to recoup the outstanding debt.

- Financial Hardship: Defaulting on payments can lead to financial hardship and stress, affecting your overall financial well-being.

Closing Summary

- Meaning, Example")

In conclusion, understanding how to access your home equity through a line of credit in Australia is a significant financial decision that requires careful consideration and planning. By following the steps Artikeld in this guide, individuals can make informed choices that align with their financial goals and aspirations.

FAQ

What is the eligibility criteria for accessing home equity in Australia?

To access home equity in Australia, individuals typically need to have a stable income, good credit history, and a sufficient amount of equity built up in their property. Lenders may also consider other factors such as the loan-to-value ratio.

What documentation is needed to apply for a line of credit?

Commonly required documents include proof of income, identification documents, property details, and financial statements. Lenders may request additional documents based on individual circumstances.

What are the consequences of defaulting on payments for a line of credit?

Defaulting on payments for a line of credit can lead to foreclosure, where the lender may seize the property used as collateral. It can also negatively impact the individual's credit score and financial stability.

{kind=link}